While 2020 dramatically shifted how people work, 2021 brought continued change as different forces in the labor market took effect. Unemployment rates have returned to pre-pandemic levels and unemployment stimulus has run its course, but employers continue to face challenges filling open positions. The Great Resignation began in 2021, and employers have increased reliance on HCM solutions to help retain and bolster their workforce.

In 2021 the HCM segment experienced record M&A activity, VC investments and IPOs, with activity accelerating into year end. The number of M&A transactions in Q4 increased 40% above Q3, with the largest rise occurring within Talent Acquisition and Core HR. VC investments increased over fivefold compared with 2020. The 2021 investment in wellness and learning companies alone exceeded the total capital raised in 2020 for all HCM segments. Finally, HCM IPO activity quadrupled relative to both 2019 and 2020. The capital flowing into the space has not only bolstered balance sheets for continued consolidation, but also for accelerated technology innovation as players strive to solve for complex macro-economic challenges. Here are five sub-sectors that saw transformative transaction activity in 2021:

Screening and Assessments: Global talent shortages have ignited the need for assessment and screening tools, as companies scramble to streamline screening, improve candidate experience and decrease hiring time. Consolidation in the background screening space was headlined by acquisitions where both Equifax and TransUnion expanded their capabilities in people data. Three of the largest background screening players completed IPOs in 2021, and three background screening firms partnered with new financial sponsors in Q4. Assessment providers joined broader talent acquisition platforms throughout the year, and VC investors continued to fund innovative pre-hire assessments.

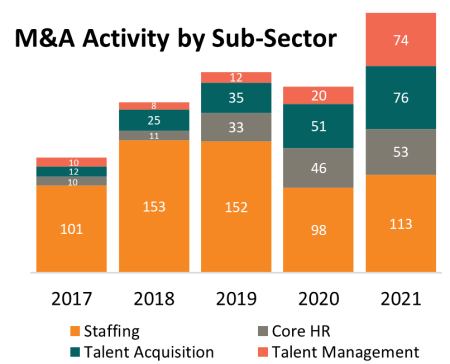

Staffing: High-margin focus and selectivity defined the staffing M&A rebound in 2021. In an effort to become “one-stop shops,” active consolidators folded in digital transformation or specialized enterprise consulting firms. The year, we also saw non-staffing companies vertically integrate by partnering with staffing firms to improve their talent acquisition efforts and combat labor scarcity. Staffing remains a seller’s market (for now) with M&A activity generally being led by PE-owned strategic buyers seeking to scale their existing platforms and create value for future exits.

Employee Engagement: Employee engagement has remained an increasingly important strategy for retaining workers and communicating across a virtual or hybrid workforce. Culture and feedback software vendors quickly consolidated this year, led by Workday’s acquisition of Peakon. Employee engagement also continues to receive VC interest, as evidenced by an increase of nearly 3x over 2020’s capital flows.

Learning & Development: Upskilling and reskilling workers is a continuing theme as accelerating digital transformation widens the skills gap for many workers. E-learning and LMS platforms continue to lead the learning market, but new disruptors in the space are starting to get noticed, particularly in the coaching world. Coaching platforms are being leveraged as a way to upskill existing employees to fill talent gaps. E-learning platforms raised nearly $2B in funding this year (60%+ of overall learning investments), followed by digital coaching solutions ($620M raised).

Corporate Wellness: The wellness space received more VC funding in 2021 than in the combined 5 years prior. Although physical health is an obvious component, especially during a pandemic, the definition of wellness is expanding. Mental health and wellbeing tools were strengthened with the $3B merger of Headspace and Ginger, and the importance of financial wellness was highlighted as on-demand pay platforms received over $1B in funding. Consolidation within employee safety training and compliance continues as investors value regulatory mandates.

We expect consolidation and investment in Human Capital solutions to remain strong in 2022. Labor market challenges are likely to persist, and employers will seek to improve hiring, engagement, development, and wellness of their employees.

DISCLAIMER This presentation is intended for information and discussion purposes only and does not constitute legal or professional investment advice. Statements of fact and opinions expressed are those of the participants individually and, unless expressly stated to the contrary, are not the opinion or position of Harbor View Advisors, LLC (“HVA”). The information in this presentation was compiled from sources believed to be reliable for informational purposes only. HVA does not endorse or approve, and assumes no responsibility for, the content, accuracy or completeness of the information presented.