We attended the annual Mortgage Bankers Association (“MBA”) conference in Nashville, TN, this past week. The conference scene is back in full swing as we had three days full of meetings where the key theme was getting through these doldrums, however long they may last. For perspective, the US residential mortgage market is in full reset as the refi market has collapsed pulling mortgage volumes down nearly 50% YOY1. The consensus seems rational but cautious as we are all asking each other when things will turn around because, in the words of one, “we aren’t there yet.”

On the M&A front, the key takeaways from our conversations with CEOs and heads of Corp Dev:

Stay core: Buyers have narrowed their M&A focus to their core business model – there is a broader theme in M&A taking hold, when end-market growth dries up, investors turn away from platform plays to more add-on transactions. They are staying to their core customers and markets and looking to use M&A to make up from lost ground on growth.

Exit noncore: Carveouts are likely to pick up – our team at Harbor View is working on two corporate carve outs as our clients seek to consolidate their focus on their core markets. Buyer’s advantage: The more aggressive buyers see valuation multiples coming down and are seeking market share and expanding tech capabilities for less. Notably, the highflyers that were trading at +10x revenue a year ago, have ratcheted back to 2-3x revenue and a willingness to roll more equity on the future market turn.

At odds: As is typical in a cyclical market during the down stroke, finding the clearing price gets tougher as the dynamics between peak and trough earnings and multiples takes time and creative negotiation to bridge. For financial buyers, the current state is made worse by M&A lenders tightening down on their underwriting thresholds.

M&A terms getting stretched: Participants are seeing a wider range of valuation proposals. Buyers that were willing to pay peak multiples a year ago are simply staying on the sidelines. In contrast, those buyers that did not get something done before the music stopped remain on the hunt but looking for bargains.

Surprisingly positive outlook: Unlike 2008 when the housing market was the culprit in the end-of-the-world-scenarios, this time around, the negative factors are more indirect – inflation, supply chain and interest rates. We see three trends going into 2023:

Consolidation: Many segments of the mortgage solutions market are ripe for consolidation and lower valuations should bolster M&A activity, particularly at the larger, more mature (less risky) end of the markets – think ICE/Ellie/Black Knight.

The race to add-on: While new platform investments have slowed, add-ons are a great substitute for organic end market growth.

COVID’s long tail: The pandemic created many new streams that should continue to gather momentum including automation in mortgage, the benefits of virtual solutions (e.g. notary signing solutions), and an openness to experiment with new models that take advantage of a remote workforce (while adapting to “the big quit”).

Bottom line, we expect the MortgageTech M&A market to continue to be active into 2023, despite being on the down stroke of the mortgage cycle. Other studies confirm this pattern – with consulting firm BCG commenting on the broader M&A market, “the level of M&A activity in 2022 is in line with recent pre-pandemic levels, despite slowing down relative to 2021’s frenzied pace.”2

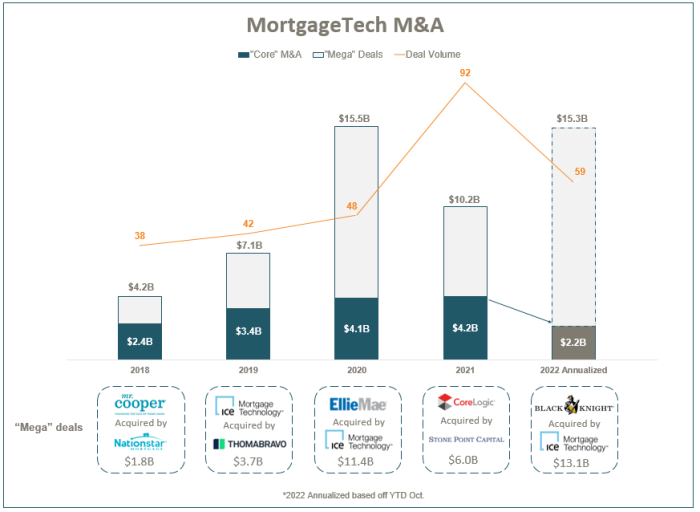

In MortgageTech, the focus has shifted away from new platform deals to more add-on and tuck-in sized acquisitions along with corporate carve outs and divestitures. We expect deal count this year will be down from last year’s spike, but still higher than the prior four years as acquirers seek out ways to consolidate through this downturn.

Transaction values include large ‘mega’ transactions such as:

DISCLAIMER This presentation is intended for information and discussion purposes only and does not constitute legal or professional investment advice. Statements of fact and opinions expressed are those of the participants individually and, unless expressly stated to the contrary, are not the opinion or position of Harbor View Advisors, LLC (“HVA”). The information in this presentation was compiled from sources believed to be reliable for informational purposes only. HVA does not endorse or approve, and assumes no responsibility for, the content, accuracy or completeness of the information presented.