In our last quarterly report, we asked the question, “Is the staffing industry back?”. Well, the answer is … somewhere between “sort of” and a very qualified “yes”. The 2026 Staffing Industry Analysts (SIA) Executive Forum in Austin painted a picture of a market that is stabilizing – but far from fully recovered and still undergoing fundamental transformation. While macro indicators are improving and sentiment is turning more positive, structural shifts driven by a stagnant labor market and technology disruption are redefining how staffing firms grow and how they are evaluated by potential acquirers.

A Market That Is Stabilizing – But Not Surging

At a macro level, the outlook for 2026 is constructive. GDP is expected to grow approximately 2.5%, inflation is moderating toward 2.4%, and there is potential for opportunistic interest rate cuts – all supportive conditions relative to the volatility of the past two years. Yet beneath the surface, the labor market tells a more complex story. Quit rates, hiring rates, and job openings are all stagnant. Hiring activity has effectively reset to levels last seen in 2014, creating what many speakers described as a “slow and static” environment.

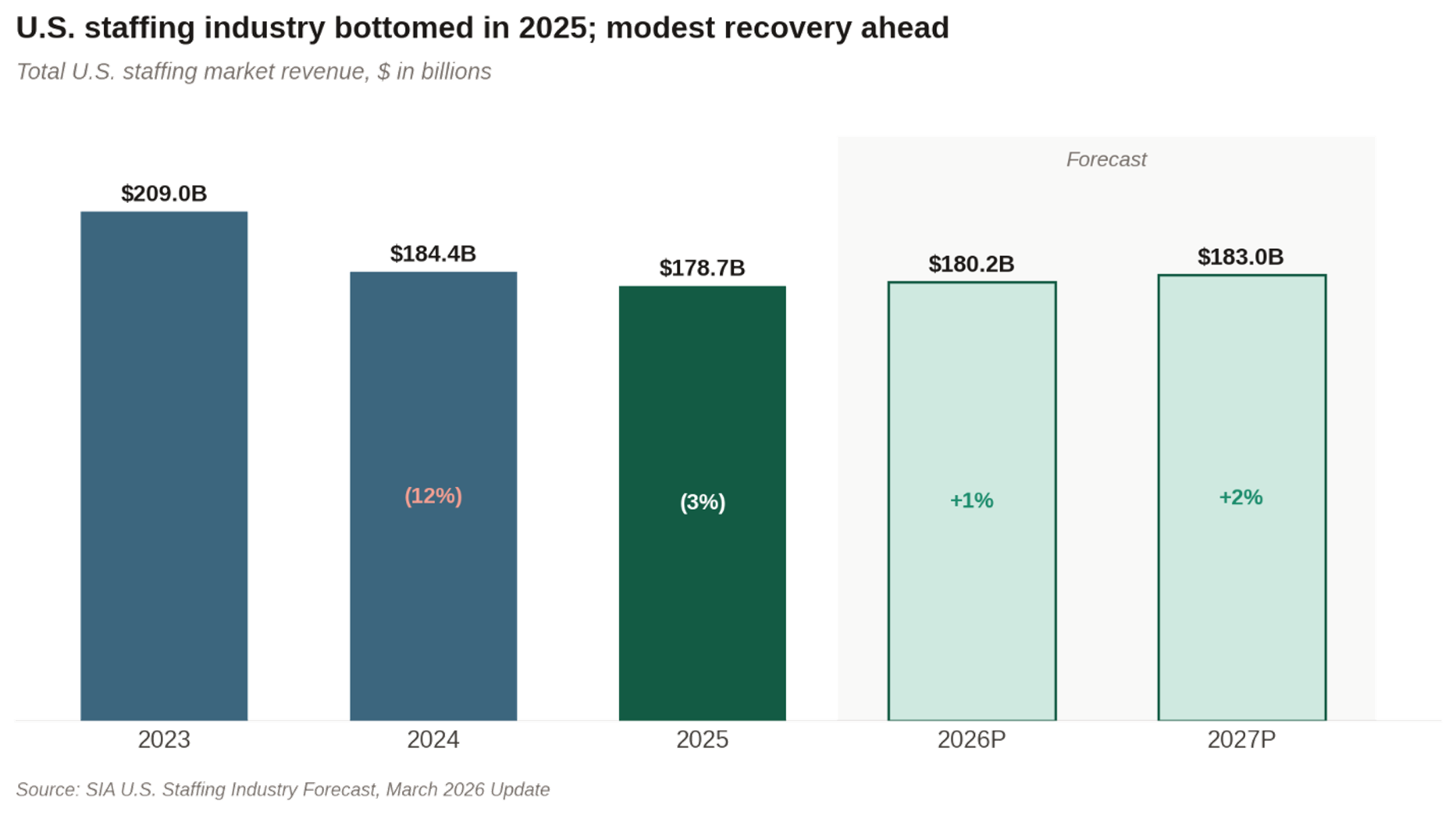

Staffing demand is not driven purely by job growth – it is also driven by labor churn. When hiring slows, churn declines, and so does demand for staffing services. As a result, even in a stable macro environment, the staffing industry has struggled to regain momentum, and the numbers reflect this dynamic. The U.S. staffing industry declined approximately 3% in 2025 to $178.7 billion. Growth is expected to return in 2026 and 2027, but only modestly, at around 1% to 2% annually. So, while the industry appears to have reached a bottom, a sharp rebound is unlikely while a static labor market persists. A meaningful recovery would likely require a resumption of labor market churn – where employees feel confident enough to change jobs and employers compete more actively for talent – alongside a steadying of client decision-making around AI's workforce impact.

Industry Divergence and the Changing Rules of the Game

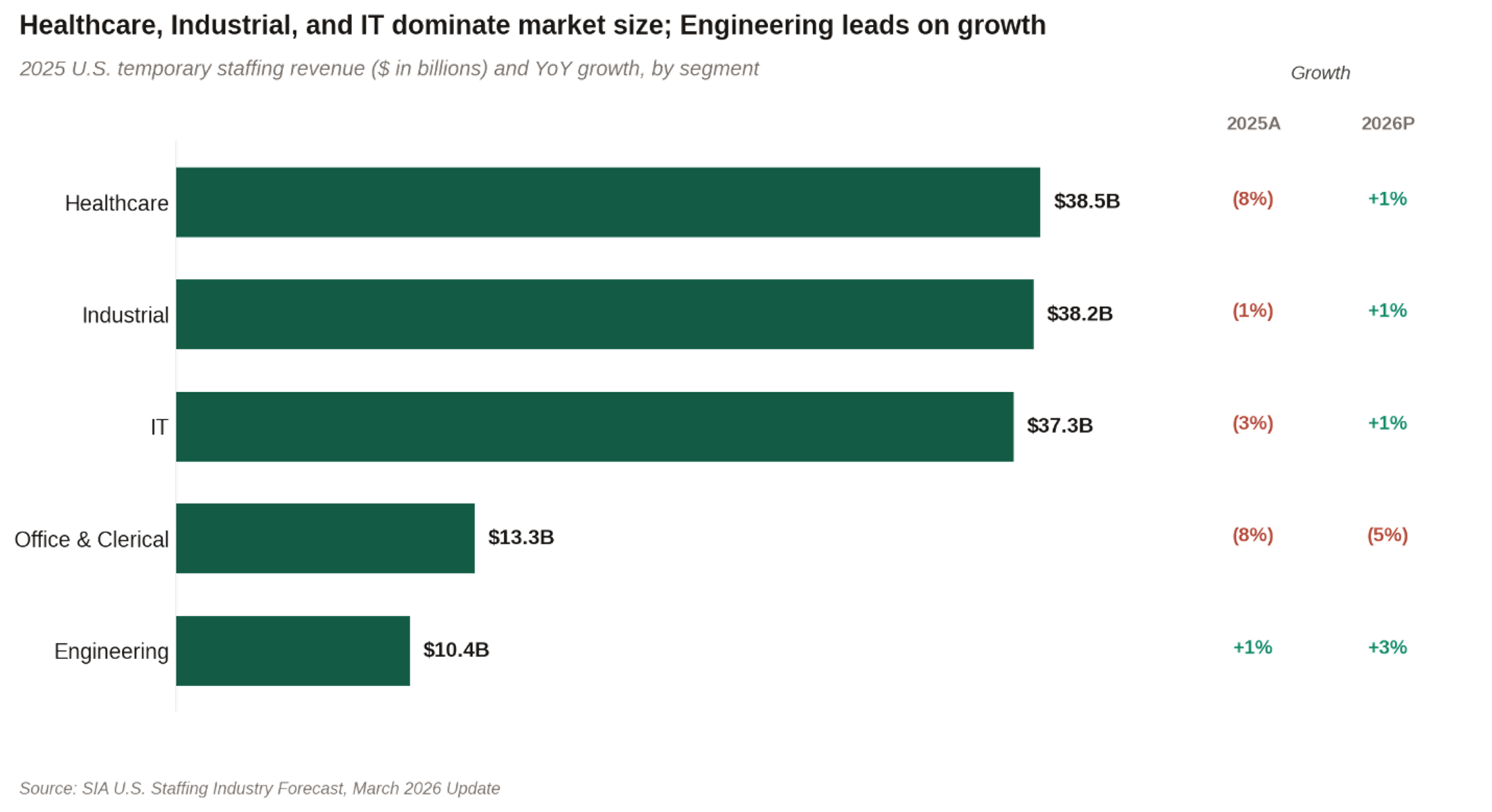

One of the clearest themes from the conference was the increasing divergence across staffing segments. The industry is no longer moving as a collective – performance is increasingly dictated by sector dynamics and technology adoption.

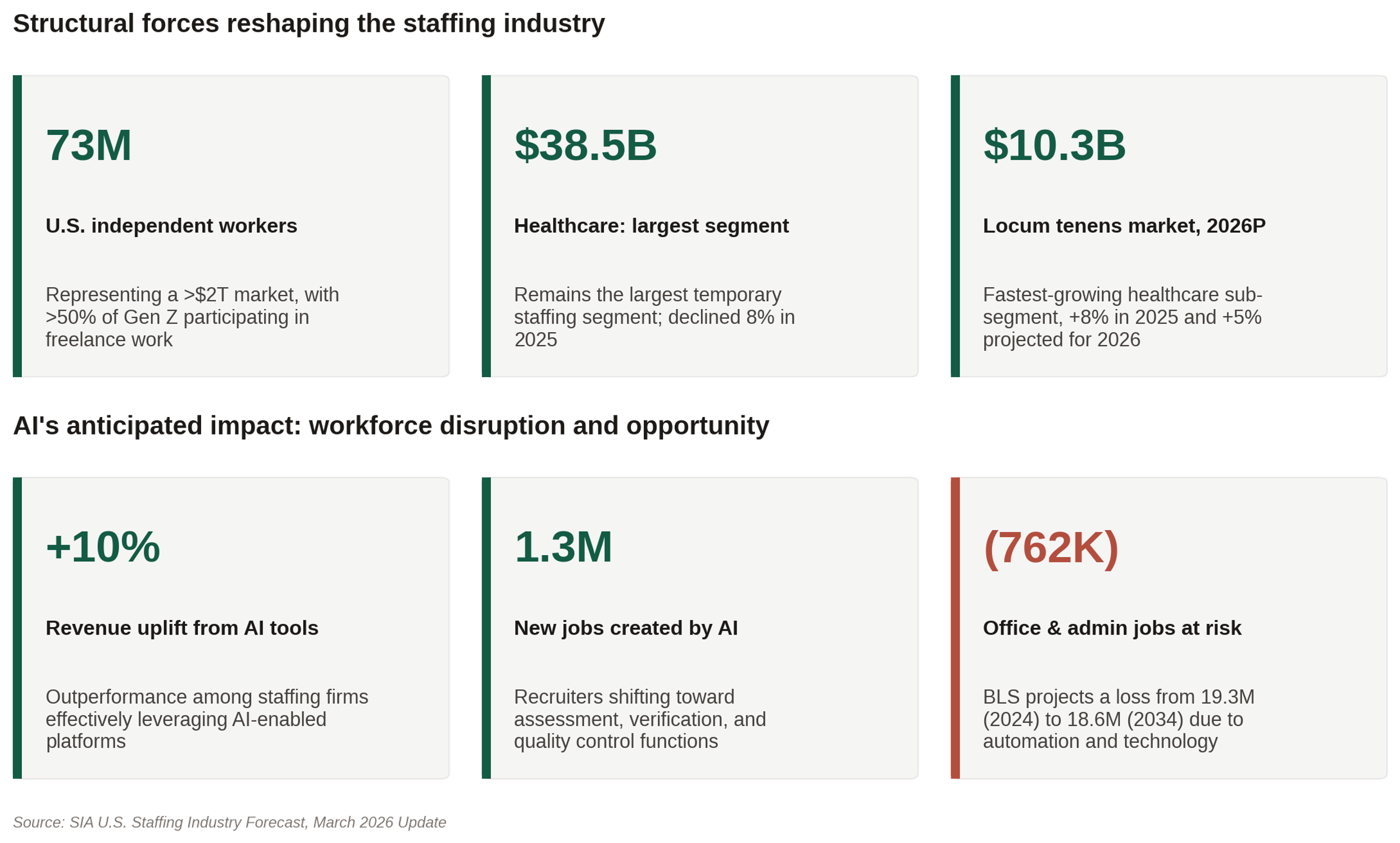

Healthcare remains the largest temporary staffing segment at $38.5 billion, though it declined 8% in 2025 as volumes continued normalizing from pandemic peaks. Within Healthcare, locum tenens stands out as the fastest-growing sub-segment, growing 8% in 2025 and projected to reach $10.3billion in 2026, driven by persistent physician shortages in key specialties.

Pockets of Industrial Staffing – particularly skilled trades, commercial driving, and energy-related construction – outperformed the broader segment, which declined only 1% in 2025, beating SIA's prior forecast of a 3% decline. Engineering staffing also returned to growth (+1%), with data center and power infrastructure projects emerging as significant demand drivers. Both segments are projected to continue growing modestly in 2026 (Industrial +1% and Engineering +3%).

IT staffing declined 3% in 2025 to $37.3B, slightly worse than the 2% decline forecast in September, as the segment continued to face headwinds from increasing offshoring, federal spending cuts, AI-assisted coding reducing demand for lower-level roles, and an ongoing shift from traditional IT staffing to IT solutions projects. The market is forecasted to return to modest 1% growth in both 2026 and 2027, supported by demand for AI / ML, data and analytics, and cloud architecture roles.

By contrast, Office and Clerical Staffing continues to decline and is the only major segment projected to contract in 2026 (-5%). Automation, government spending cuts, and changing workplace dynamics (more cost-efficient virtual workforces, etc.) are resulting in reduced demand for traditional administrative roles. The long-term outlook is that this is unlikely to reverse, with the Bureau of Labor Statistics projecting a loss of 762,000 office and administrative support jobs over the next decade due to technology and automation.

For operators and investors alike, the implication is clear: generalist staffing is less valuable than targeted specialization, and exposure to durable demand drivers is essential in an environment characterized by business cyclicality and ongoing technological upheaval.

AI Disruption and Resulting Opportunities for Staffing Firms

AI was a central theme throughout the forum, though conversation has become more focused on action and outcomes compared to the speculative tone seen in prior years. In the past few months, AI has caused significant disruption – particularly in the technology sector. The so-called “SaaSpocalypse” has led to widespread layoffs, and many companies remain hesitant to hire. As a result, there is little expectation of a near-term rebound in tech hiring. However, the longer-term outlook is more nuanced. AI has already created approximately 1.3 million new jobs, and conference speakers emphasized its potential to unlock new job opportunities versus simply displace them. Rather than eliminating staffing demand, AI is likely to change where and how value is created within the staffing ecosystem.

Recruiters, for example, are expected to shift away from traditional sourcing toward more complex functions such as candidate assessment, verification, and quality control. AI can automate outreach and initial screening, but it also introduces new challenges – most notably, an increase in fraudulent candidate profiles and resume inflation. This dynamic increases friction in the hiring process, which paradoxically makes staffing firms more essential. Additionally, firms that effectively leverage AI-enabled tools and platforms are outperforming their peers, with data suggesting roughly 10% higher revenue performance among firms embracing these technologies. The firms that will exhibit the most resilience will be those that integrate technology into their workflows while maintaining a strong human layer where it matters most.

Structural Shifts in the Labor Market

Beyond current economic, sector, and technology dynamics, several long-term factors are reshaping the labor market in ways that will have lasting implications for staffing. The aging population remains one of the most powerful drivers of demand, particularly in healthcare, but also in senior services and adjacent industries. Additionally, the rise of the independent workforce continues to accelerate. Today, there are approximately 73 million independent workers in the United States, representing a market exceeding $2 trillion. Notably, more than half of Gen Z workers are already participating in freelance or independent work. Staffing firms with exposure to favorable demographic trends – and the ability to effectively engage and manage a growing independent talent pool – are well positioned to foster meaningful competitive differentiation.

Corporate hiring priorities are also evolving. For instance, large technology organizations (e.g., Amazon, Meta, Dell, Oracle) are reallocating resources away from traditional IT, R&D, and engineering roles, while selectively investing in areas tied to AI deployment, data management, operational efficiency, and business development. This reflects a broader mindset transition from growth-at-all-costs to profitability and optimization, resulting in a low-fire, low-hire environment where companies prioritize productivity over expansion. This shift is creating a more selective demand landscape, requiring staffing firms to demonstrate clear ROI and position themselves as partners in creating efficiencies rather than just providing incremental headcount.

The “Uncertainty Tax” and Its Ripple Effects

Geopolitical risk, particularly the ongoing Iran conflict, was another recurring theme at SIA. While there has been no measurable impact on staffing data to date, the potential implications are significant. If the conflict persists, industrial-focused companies (with exposure to trade, logistics, etc.) would likely be impacted first, with broader spillover effects across the economy. Rising energy prices also pose a risk to infrastructure buildouts, including data centers, given the high energy requirements of AI.

However, the more immediate impact is psychological, as uncertainty itself is acting as a constraint. Organizations are delaying hiring decisions, investors are exercising greater caution, and transaction timelines are extending. Even in the absence of concrete economic disruption, this “uncertainty tax” is influencing behavior across the market.

Implications for M&A in 2026

Against this backdrop, M&A activity in the staffing sector is showing signs of recovery. Anecdotally, company performance is generally up 5–10% year-to-date compared to last year, sentiment is improving, and more firms are willing to consider their options with potential acquirers. However, as is the case with all industries, the recovery in M&A is uneven and highly selective. Buyers are prioritizing segments with exposure to durable growth levers such as Healthcare, Industrial, and Engineering Staffing. At the same time, there is increased scrutiny around revenue quality (growth and repeatability), earnings quality (Gross and EBITDA margins), customer concentration, exposure to cyclicality, and AI integration roadmaps.

Strategic fit is also becoming more important than scale. Acquirers are increasingly focused on capability expansion, vertical specialization, and technology enablement rather than simple revenue aggregation. Process dynamics are evolving as well. Transactions are taking longer to complete, diligence is more rigorous, and buyers are more disciplined. However, capital remains available, and private equity firms continue to face pressure to deploy, providing underlying support for deal activity. Strategics also are still focused on M&A as a key part of their overall growth strategies.

The overarching takeaway from SIA’s 2026 Executive Forum is that the staffing industry is not simply just recovering – it is also transitioning. Firms that are aligned with sustainable demand drivers, embrace technology without losing the human element, and offer specialized, high-quality services will be best positioned to grow and garner attention in a selective M&A market. For investors and operators alike, the opportunity is not in waiting for a broad-based rebound – it is in identifying and acting on these new avenues for growth today.

These key takeaways reflect comments made by conference speakers, including but not limited to: Michael Schultz (Economist – Staffing Industry Analysts), Daniel Culbertson (Senior Economist – Indeed Hiring Lab), Kory Kantenga (Head of Economics, Americas – LinkedIn), Teresa Creech (President – MBO Partners by Beeline), Janette Marx (CEO – Employbridge), Art Papas (Founder & CEO – Bullhorn), Mike Small (President – Akkodis, North America), Michael Smith (Chief Executive – Randstad Enterprise), Ursula Williams (President – Staffing Industry Analysts), John Nurthen (Executive Director, Global Research – Staffing Industry Analysts).

DISCLAIMER This presentation is intended for information and discussion purposes only and does not constitute legal or professional investment advice. Statements of fact and opinions expressed are those of the participants individually and, unless expressly stated to the contrary, are not the opinion or position of Harbor View Advisors, LLC (“HVA”). The information in this presentation was compiled from sources believed to be reliable for informational purposes only. HVA does not endorse or approve, and assumes no responsibility for the content, accuracy or completeness of the information presented.